Yes, it is possible to have a cosigner on a VA loan. A cosigner can help increase your chances of approval and may also help you qualify for a larger loan amount.

VA loans are backed by the Department of Veterans Affairs and are designed to help veterans, active-duty service members, and their families buy homes. These loans have many benefits, including no down payment requirement and no private mortgage insurance. However, VA loans also have strict eligibility requirements, including a minimum credit score and income threshold.

If you are unable to meet these requirements on your own, having a cosigner may be a good option. In this blog post, we will explore the details of having a cosigner on a VA loan and what you need to know before considering this option.

Eligibility Criteria For Va Loans

When it comes to VA loans, having a cosigner can be a viable option for individuals who may not meet the eligibility requirements on their own. In this article, we will delve into the eligibility criteria for VA loans, including the qualifying service requirements and credit and income assessments.

Qualifying Service Requirements

To be eligible for a VA loan, service members must have served for a minimum period of 90 consecutive days during wartime or 181 days during peacetime. National Guard and Reserve members may qualify after serving for at least six years, unless called to active duty sooner. Spouses of service members who died in the line of duty or as a result of a service-related disability may also be eligible.

Credit And Income Assessments

Credit score requirements for VA loans are generally more flexible than those for conventional loans. While there is no official minimum credit score, most lenders prefer a score of at least 620. Additionally, income stability is crucial, and lenders typically assess the borrower’s debt-to-income ratio to ensure they can comfortably afford the loan.

The Role Of A Cosigner

Cosigner Responsibilities

A cosigner on a VA loan agrees to take on the financial responsibility if the primary borrower defaults.

Benefits Of Adding A Cosigner

- Increased chances of loan approval

- Lower interest rates

- Enhanced borrowing capacity

Va Loan Cosigning Explained

When applying for a VA loan, having a cosigner can be beneficial for borrowers who may not meet all the requirements on their own. Understanding the implications of having a cosigner on a VA loan is essential for both the borrower and the cosigner.

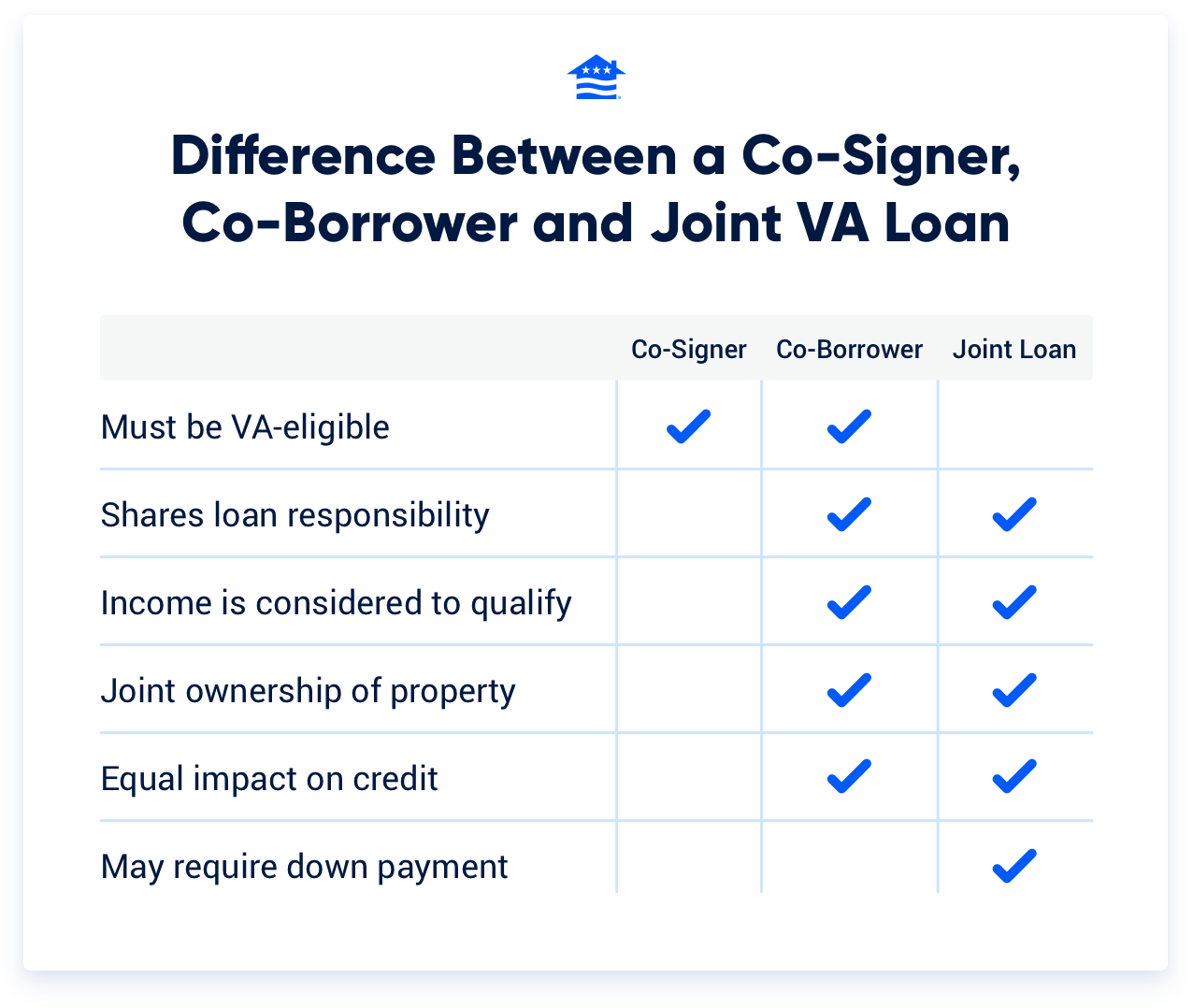

Cosigner Vs. Co-borrower Distinction

A cosigner is someone who agrees to repay the loan if the borrower defaults, while a co-borrower is equally responsible for the loan and shares ownership of the property.

Cosigning Affects Loan Approval

Having a cosigner with strong credit and income can increase the chances of loan approval, as it reassures lenders about the borrower’s ability to repay the loan.

Cosigner Eligibility For Va Loans

Having a cosigner on a VA loan is possible, but not always necessary. Eligibility requirements for cosigners include being a spouse, veteran, or active-duty service member. Additionally, they must meet income and credit score criteria.

Cosigner Qualifications

In certain situations, a borrower may consider having a cosigner for a VA loan. The cosigner must be a close relative of the borrower, such as a spouse or a parent. The cosigner’s income and credit score can help the borrower qualify for the loan. However, the cosigner cannot be a non-occupying co-borrower on the loan application.Restrictions And Limitations

It’s important to note that while a cosigner can assist the primary borrower in qualifying for a VA loan, the Department of Veterans Affairs does not officially recognize cosigners. This means that the cosigner’s income can only be used to help the borrower meet the VA’s debt-to-income ratio requirements. The cosigner will not have ownership interest in the property unless they are also listed as a co-borrower on the loan. When considering a cosigner for a VA loan, it’s essential to understand the qualifications and limitations associated with this arrangement. The cosigner must be a close relative of the borrower and their income can only be used to help meet the debt-to-income ratio requirements.Impact On The Veteran

Having a cosigner on a VA loan can impact the veteran in various ways. While it can increase the chances of loan approval, the veteran and cosigner share equal responsibility for the loan, including repayment and consequences of default. It’s essential to consider all factors before deciding to add a cosigner to your VA loan.

Loan Entitlement Implications

Debt-to-income Ratio Considerations

Credit: veteran.com

Risks For The Cosigner

When considering a VA loan with a cosigner, it’s important to understand the risks involved. While having a cosigner can help you qualify, they are equally responsible for the loan, and any missed payments can affect their credit. It’s crucial to have a clear understanding of the implications for both parties involved.

Liability In The Event Of Default

A cosigner on a VA loan is equally responsible for payments if the borrower defaults.

Long-term Credit Implications

Cosigning affects the credit score and ability to secure loans in the future.

Alternative Solutions

For those who don’t have a cosigner, there are alternative solutions available to secure a VA loan. These solutions can help individuals navigate the homebuying process without a cosigner’s support.

Joint Va Loans

Joint VA loans allow eligible individuals to apply for a VA loan with another person. Both applicants must meet VA requirements, ensuring shared responsibility for the loan.

Secondary Financing Options

Secondary financing options can also be explored for those without a cosigner. These options include personal loans, grants, or down payment assistance programs.

Navigating The Application Process

When applying for a VA loan, having a co-signer can be a viable option for individuals who may not meet the credit or income requirements on their own. Navigating the application process with a co-signer involves understanding the required documents, procedures, and tips for a smooth approval.

Documents And Procedures

When including a co-signer on a VA loan application, specific documents are necessary to validate their financial standing and willingness to assume responsibility for the loan. These may include:

- Co-signer’s income verification

- Co-signer’s credit history

- Co-signer’s identification

Additionally, the application procedures for including a co-signer typically involve providing the co-signer’s information at the onset of the loan application and ensuring that all required documents are accurately submitted to the lender.

Tips For A Smooth Approval

To enhance the chances of a smooth approval with a co-signer, consider the following tips:

- Choose a co-signer with strong credit and stable income

- Communicate openly with the co-signer about their responsibilities

- Ensure all required documents are prepared and submitted accurately

Legal And Financial Advice

Legal and financial advice is crucial when considering a cosigner for a VA loan. Consulting with experts and understanding the fine print are essential steps in this process.

Consulting With Experts

Before proceeding with a cosigner on a VA loan, seek advice from legal and financial professionals. They can provide insights on the implications and obligations involved.

Understanding The Fine Print

Review the loan agreement thoroughly to grasp the responsibilities of both the primary borrower and the cosigner. Ensure transparency and clarity in all terms and conditions.

Credit: m.youtube.com

Real-life Scenarios

Success Stories

With a VA loan, having a cosigner can make homeownership dreams a reality for many individuals. Take the case of John, who was able to secure a VA loan with his father as a cosigner. This allowed John, a veteran struggling with a lower credit score, to purchase his first home. The support of his father as a cosigner not only helped John qualify for the loan, but also secured a lower interest rate, making the home purchase more affordable for him.

Cautionary Tales

Conversely, there are cautionary tales to consider when it comes to having a cosigner on a VA loan. Sarah, a military spouse, faced challenges when her cosigner experienced financial difficulties, leading to complications with the loan. Despite Sarah’s strong credit history and income, the lender required her to find a new cosigner or secure the loan independently, causing significant stress and delays in the home buying process.

Credit: www.veteransunited.com

Frequently Asked Questions

Can You Have An Unmarried Co-borrower On A Va Loan?

Yes, you can have an unmarried co-borrower on a VA loan. Both individuals must meet eligibility requirements.

Can A Girlfriend Be On Title On A Va Loan?

Yes, a girlfriend can be on the title of a VA loan if she is a co-borrower and meets the eligibility requirements.

Will I Get Approved If I Have A Cosigner?

Having a cosigner can increase your chances of approval for a loan. Lenders feel more secure with a cosigner’s additional guarantee.

Can I Use My Dad’s Va Loan?

Yes, you can use your dad’s VA loan if you meet eligibility requirements. Contact a VA-approved lender for details.

Conclusion

Having a cosigner for a VA loan can open up opportunities for those who may not meet the eligibility requirements on their own. It’s important to carefully consider the responsibilities and potential benefits of involving a cosigner in your VA loan application.

Understanding the implications and seeking professional advice can help you make an informed decision.